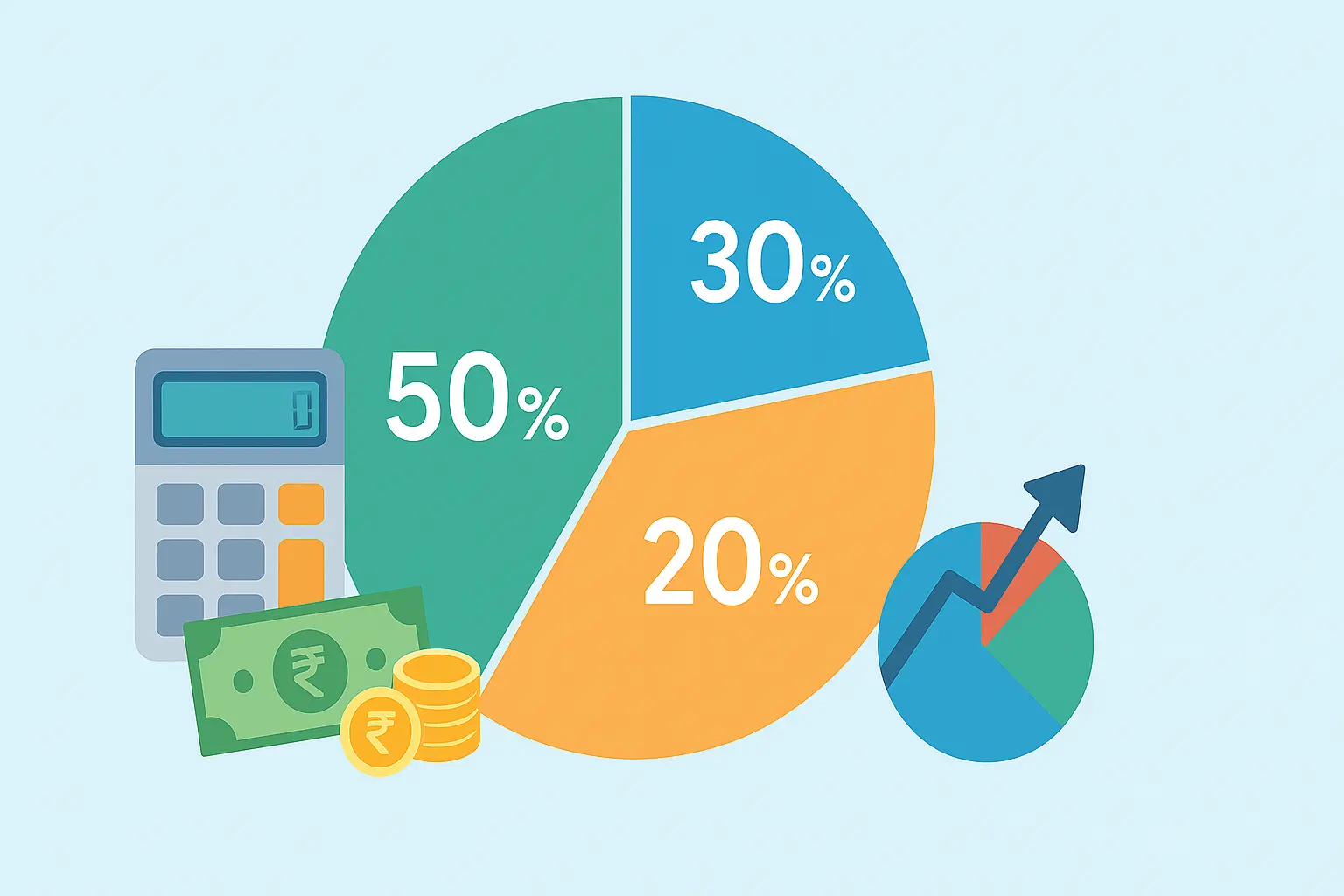

The 50-30-20 rule is a simple budgeting framework that divides your net monthly income into three buckets: 50% for needs, 30% for wants, and 20% for savings & debt repayment. It’s easy to remember and practical for people starting their financial journey. This India-focused guide explains how to apply the rule, adapt it for different incomes and cities, provides real examples and a handy interactive calculator to visualise your monthly allocation.

The rule is a guideline — not a one-size-fits-all law. Use it as a starting point and customise based on housing costs, family responsibilities, or aggressive debt repayment goals.

What Each Bucket Means

Needs — 50%

Needs are essential expenses you must pay to live and work: rent or EMI, groceries, utilities, essential transport, healthcare, minimum loan payments and compulsory insurance premiums.

Wants — 30%

Wants are discretionary: dining out, travel, subscriptions, entertainment, hobbies and non-essential upgrades.

Savings & Debt Repayment — 20%

This bucket includes building an emergency fund, investing through SIPs or lumpsum, retirement savings and extra loan prepayments above minimum EMIs.

Why the 50-30-20 Rule Works

- Simple to follow: No complex categories — easy mental model for everyday decisions.

- Helps automate: You can set fixed transfers for savings and needs and let wants be flexible.

- Psychologically sustainable: Allows room for fun so you don’t feel deprived.

When to Follow It — and When to Modify

Apply the rule as-is if you are building basic financial discipline. Modify if:

- Housing costs in your city exceed 25% of income — reduce wants or increase income.

- You have high-interest debt — allocate more than 20% to accelerate repayment.

- You are saving for a near-term target (house downpayment) — temporarily increase savings to 30–50%.

- Your income is irregular — use a conservative baseline (lowest 3-month average) to avoid shortfalls.

50-30-20 Interactive Calculator

Enter your monthly take-home income below to instantly see suggested allocations. You can also set a custom savings percentage and compare with the 50-30-20 guideline.

50-30-20 Calculator

Real-Life Examples (India)

Example 1 — Young professional, ₹40,000 net

- Needs (50%): ₹20,000 — rent ₹9,000, groceries ₹5,000, transport/utility ₹3,000, insurance/EMI ₹3,000

- Wants (30%): ₹12,000 — dining out, OTT subscriptions, shopping

- Savings (20%): ₹8,000 — emergency fund + SIP

Example 2 — Family in a metro, ₹100,000 net

With higher housing and education costs, family budgets may look like: Needs 60%, Wants 20%, Savings 20% (temporary). Aim to restore savings to 20%+ over time by increasing income or trimming wants.

Variations & When to Break the Rule

Some useful alternatives:

- Aggressive saver: 40-30-30 (more to savings)

- Debt-focused: 50-20-30 (more to debt repayment within savings bucket)

- High-cost city: 60-20-20 temporarily

- Irregular income: use a conservative baseline and keep a larger emergency fund

How to Make the Rule Work — Practical Tips

- Automate savings: standing instruction to transfer to savings/SIP on payday.

- Track weekly: small reviews avoid month-end surprises.

- Cut one subscription per month: quick wins add up.

- Use virtual buckets: separate accounts or app tags for goals.

- Increase savings with raises: route a portion of raises to savings first.

Common Mistakes to Avoid

- Using gross instead of net income for calculations.

- Counting long-term investments as “available” for monthly wants.

- Not accounting for irregular annual expenses (insurance renewals, maintenance).

30-Day Action Plan — Implement the 50-30-20 Rule

- Calculate your net income and set up a savings transfer for 20%.

- List fixed monthly needs and automate bill payments.

- Track variable spends for one month and categorise into wants/needs.

- Cancel one unused subscription and move the money to your savings bucket.